Even after you learn how to create your first budget, you’ll face some challenges. Here’s how to overcome the most common ones:

Do you ever get to the end of the month and wonder where all your money went? You’re not alone. Nearly 65% of Americans don’t know how much they spent last month, according to the National Financial Educators Council. The truth is, without a budget, your money controls you instead of the other way around.

Creating your first budget might sound intimidating, but it’s actually one of the simplest and most powerful things you can do for your financial health. If you’re new to managing money, start with our beginner’s guide to personal finance to build a solid foundation. In this guide, you’ll learn exactly how to create your first budget from scratch, even if you’ve never tracked a single expense before. By the end, you’ll have a clear plan that helps you save money, reduce stress, and finally feel in control of your finances.

Why You Need to Create Your First Budget (Even If You Think You Don’t)

Before we dive into the how-to, let’s address the elephant in the room. Many people resist budgeting because they think it means giving up the things they love or living on rice and beans. That couldn’t be further from the truth.

When you learn how to create your first budget, you’ll realize it’s simply a plan for your money. It tells your dollars where to go instead of wondering where they went. With a budget, you can still enjoy your daily coffee or weekend outings—you just do it intentionally, without the guilt or financial stress.

Here’s what a good budget actually does for you:

- Shows you exactly where your money is going each month

- Helps you find “money leaks” you didn’t know existed

- Gives you permission to spend on things you value

- Reduces financial stress and arguments about money

- Helps you save for goals that matter to you

Think of budgeting like using GPS for a road trip. You wouldn’t drive across the country without directions, right? Your budget is your financial GPS.

Step 1: Calculate Your Monthly Income

When learning how to create your first budget, the foundation starts with knowing exactly how much money you have coming in each month. This sounds simple, but it’s crucial to get this number right.

For salaried employees: Look at your take-home pay (after taxes, insurance, and retirement contributions). If you’re paid biweekly, you typically receive two paychecks per month, so add those together. Remember that two months per year have three paychecks—you can treat those as “bonus” months.

For hourly workers or irregular income: Calculate an average based on the last three to six months. It’s better to underestimate than overestimate here. If your income varies significantly, use the lowest month as your baseline.

Don’t forget to include:

- Side gig income (looking to boost your earnings? Check out our guide on the best side hustles to start today)

- Freelance payments

- Child support or alimony

- Investment dividends

- Any other regular income sources

Write this number down. This is your starting point, and everything else in your budget will flow from this total.

Step 2: Track Your Current Spending

You can’t improve what you don’t measure. Before you create spending categories, you need to understand your current habits. This step is eye-opening for most people—you’ll likely discover you’re spending way more than you thought in certain areas.

Here’s how to track effectively:

Gather your last three months of bank statements and credit card bills. Go through each transaction and sort them into basic categories. Don’t overthink this—you’ll refine categories later.

Start with these broad categories:

- Housing (rent/mortgage, utilities, insurance)

- Transportation (car payment, gas, insurance, maintenance)

- Food (groceries and dining out)

- Insurance (health, life, etc.)

- Debt payments

- Personal spending (clothing, entertainment, subscriptions)

- Savings and investments

Use a simple spreadsheet or even a notebook. The method doesn’t matter as much as actually doing it. Add up each category and calculate your monthly average.

Pro tip: Many people are shocked to discover they spend $200+ per month on subscriptions they barely use or $400+ dining out without realizing it. This tracking exercise alone can help you identify $100-300 in potential savings. Learn more strategies in our guide to cutting unnecessary expenses and saving more each month.

Step 3: Choose Your Budgeting Method

Not all budgets are created equal, and what works for your best friend might not work for you. Here are the three most effective budgeting methods for beginners:

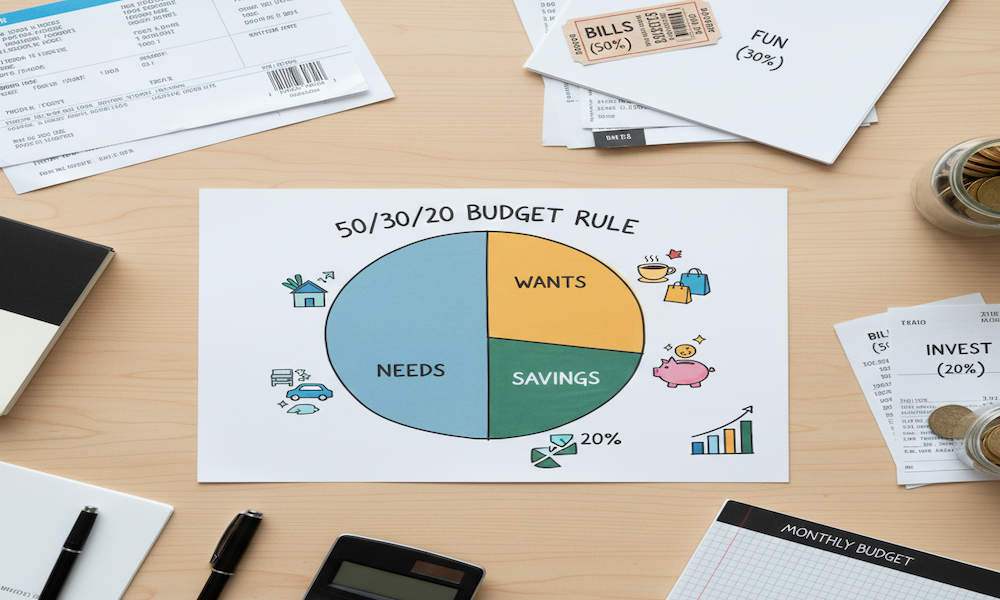

The 50/30/20 Budget (Best for Beginners)

This simple framework divides your income into three categories:

- 50% for needs: Housing, utilities, groceries, insurance, minimum debt payments

- 30% for wants: Dining out, entertainment, hobbies, subscriptions

- 20% for savings and extra debt payments: Emergency fund, retirement, paying off debt faster

This method is incredibly forgiving and easy to maintain. If you’re overwhelmed by the idea of tracking every single expense, start here.

Zero-Based Budget (Best for Detail-Oriented People)

With this method, you assign every single dollar a job until you reach zero. If you earn $3,500 per month, you allocate all $3,500 to specific categories. This doesn’t mean you spend it all—savings is a category too.

This approach gives you maximum control and awareness of your money. It requires more time and attention but delivers powerful results.

Envelope Budget (Best for Cash Spenders)

This old-school method involves withdrawing cash and dividing it into physical envelopes labeled with categories like “groceries” or “entertainment.” When the envelope is empty, you’re done spending in that category for the month.

While fully cash-based systems are less practical today, you can adapt this using separate checking accounts or budgeting apps that create virtual “envelopes.”

Choose the method that feels most sustainable for your lifestyle. You can always switch later if something isn’t working.

Step 4: Set Up Your Budget Categories

Now that you’ve chosen your method and know your spending patterns, this next step in how to create your first budget involves setting up your actual budget categories.The goal is to have enough detail to be useful without making it so complicated that you give up.

Essential categories to include:

Fixed Expenses (same amount each month):

- Rent or mortgage

- Car payment

- Insurance premiums

- Loan payments

- Subscriptions

Variable Expenses (change month to month):

- Groceries

- Utilities

- Gas

- Dining out

- Entertainment

- Personal care

- Clothing

Savings Goals:

- Emergency fund

- Retirement contributions

- Vacation fund

- Down payment savings

- Holiday shopping fund

Irregular Expenses (don’t forget these!):

- Car maintenance and repairs

- Medical co-pays

- Annual subscriptions

- Gifts for birthdays and holidays

- Home repairs

Here’s a realistic sample budget for someone earning $3,500 per month:

- Housing: $1,050 (30%)

- Transportation: $455 (13%)

- Food: $420 (12%)

- Insurance: $175 (5%)

- Debt payments: $280 (8%)

- Savings: $350 (10%)

- Personal/Entertainment: $420 (12%)

- Utilities: $175 (5%)

- Miscellaneous: $175 (5%)

Your percentages will vary based on your location, lifestyle, and goals. The key is making sure your expenses don’t exceed your income. For more guidance on managing housing costs specifically, see our tips for keeping rent and mortgage affordable.

Step 5: Adjust and Prioritize Your Spending

This is where the magic happens when you learn how to create your first budget. Now that you can see everything laid out, you’ll likely notice that your expenses exceed your income, or you’re not saving as much as you’d like. It’s time to make some strategic adjustments.

Start by asking these questions about each category:

Is this expense truly necessary right now? Some things feel essential but are actually wants in disguise.

Can I reduce this without major lifestyle changes? Maybe you can’t eliminate your grocery budget, but could you meal plan to reduce it by $100?

What am I getting in return for this spending? If you’re paying $60 for a gym membership you use twice a month, that’s $30 per visit. A better use of that money might be home workouts and a streaming fitness app.

Priority ranking system:

Put your expenses in this order:

- Basic needs (housing, food, utilities)

- Debt minimum payments

- Insurance

- Emergency savings (at least $50-100 per month)

- Transportation

- Everything else

If you need to cut spending, start from the bottom and work your way up. Never sacrifice categories one through four to fund wants.

Common areas where people find easy savings:

- Streaming services: Keep 1-2, rotate the rest ($30-50/month)

- Dining out: Cut frequency in half ($100-200/month)

- Groceries: Meal planning and shopping with a list ($50-100/month)

- Phone plan: Switch to a budget carrier ($20-40/month)

- Entertainment: Choose free or low-cost activities ($50-100/month)

Even small adjustments add up quickly. Saving $50 across six categories gives you an extra $300 per month—that’s $3,600 per year.

Step 6: Implement Your Budget

Now that you know how to create your first budget, comes the most important part: actually using it.. Many people create beautiful budgets that sit unused in a drawer. Don’t let that be you.

Choose your tracking system:

Budgeting apps like Mint, YNAB (You Need A Budget), or EveryDollar sync with your bank accounts and automatically categorize transactions. This is the easiest option for most people.

Spreadsheets give you complete control and customization. You can use Google Sheets templates or create your own. This requires more manual entry but some people prefer the hands-on approach.

Paper and pen works perfectly fine if you’re old school. A simple notebook where you write down expenses and check against your budget is totally valid.

The best system is the one you’ll actually use consistently. Start with whichever feels least overwhelming.

Weekly money dates:

Set aside 15-20 minutes once a week to review your budget. Pick the same day and time—Sunday evenings work well for many people. During this time:

- Review all transactions from the past week

- Ensure everything is categorized correctly

- Check your progress in each category

- Adjust spending for the remainder of the month if needed

This weekly check-in prevents that panicked feeling when you realize on day 28 that you’ve already blown your budget.

Be prepared for the learning curve:

Your first month will be messy. That’s completely normal. You’ll forget to budget for things, underestimate expenses, and probably overspend in a few categories. The second month will be better. By month three, you’ll have a realistic budget that actually works for your life.

Don’t aim for perfection—aim for progress.

Step 7: Review and Adjust Monthly

A budget isn’t something you create once and forget about. It’s a living document that should evolve with your life and priorities.

At the end of each month, spend 30 minutes reviewing:

What categories did I overspend in? Look for patterns. If you’ve gone over your grocery budget three months in a row, you probably need to increase that allocation.

Where did I underspend? If you budgeted $200 for entertainment but only spent $100, you can reallocate that extra $100 to savings or another category.

What unexpected expenses came up? These one-time costs should be planned for in future budgets. If you had a $300 car repair, start adding $50 monthly to a car maintenance fund.

Am I making progress toward my goals? Check your savings accounts. Are they growing? If not, what needs to change?

Adjust your budget when life changes:

Major life events require budget updates:

- Got a raise? Decide immediately where that extra money goes

- New baby? Add categories for diapers, childcare, and baby needs

- Moved to a new city? Update housing and transportation costs

- Paid off a debt? Reallocate that payment to savings or another goal

Your budget should reflect your current reality, not where you were six months ago.

Common Budgeting Challenges (And How to Fix Them)

Even with the best intentions, you’ll face obstacles. Here’s how to overcome the most common budgeting challenges:

Challenge: Irregular Income Solution: Budget based on your lowest-earning month. Any extra income becomes savings or extra debt payments. Build a larger emergency fund (3-6 months of expenses) for additional security.

Challenge: Unexpected Expenses Keep Derailing My Budget Solution: Create a “miscellaneous” or “stuff I forgot to budget for” category with $100-200. Also start building an emergency fund so car repairs or medical bills don’t destroy your progress.

Challenge: My Partner and I Can’t Agree on the Budget Solution: Schedule a monthly money meeting where you both have input. Start with shared goals you both care about, then work backward to create a budget that supports those goals. Consider having some “no questions asked” personal spending money for each person.

Challenge: I Feel Deprived Solution: Your budget should include fun money. If you love coffee, budget for it guilt-free. The point isn’t to eliminate joy—it’s to spend intentionally on what truly matters to you while cutting what doesn’t.

Challenge: I Keep Giving Up After a Few Weeks Solution: Start smaller. Don’t try to track 25 categories perfectly. Begin with just three: income, essential expenses, and everything else. You can add detail as the habit becomes easier.

Your Budget Success Checklist

Before you finish reading and get started, use this quick checklist to ensure you’re set up for success:

- [ ] Calculated exact monthly take-home income

- [ ] Tracked current spending for at least one month

- [ ] Chosen a budgeting method that fits your style

- [ ] Created realistic budget categories

- [ ] Assigned every dollar a purpose

- [ ] Set up a tracking system (app, spreadsheet, or paper)

- [ ] Scheduled weekly 15-minute money check-ins

- [ ] Planned a monthly budget review session

- [ ] Started or added to emergency fund

- [ ] Included some “fun money” to prevent burnout

Take Action Today

Learning how to create your first budget step by step is one of the smartest financial moves you’ll ever make. It gives you clarity, control, and confidence with your money. Remember, the goal isn’t perfection—it’s progress. Even a messy budget that you actually use is infinitely better than no budget at all.

Start today with just one step. Calculate your income, or download a budgeting app, or simply write down what you spent this week. Forward momentum is what matters.

What’s the biggest budgeting challenge you’re facing right now? Drop a comment below and let’s problem-solve together. If you found this guide helpful, share it with someone who’s also trying to get their finances on track.

For more money management strategies, check out our complete guide to building an emergency fund from scratch and our proven strategies for paying off debt faster. Your financial freedom journey starts with a single step—and you just took it.

Leave a Reply